AI Capex Exceeds $725B as Q1 Earnings Draw Investment Payoff Line

Amazon's free cash flow collapsed to $1.2 billion yet Alphabet surged while Microsoft and Meta fell, drawing the first clear line between AI capital spending and realized returns in Q1 2026.

seekingalpha.com

seekingalpha.com

In this article

A single line item on Amazon's Q1 2026 cash-flow statement — free cash flow, down from $26 billion a year ago to $1.2 billion — tells the story more cleanly than any earnings deck could. The company's trailing-twelve-month capex surpassed $100 billion for the first time, and the market, puzzlingly, sent the stock to record highs. The number, reported by 24/7 Wall St., captures a dynamic that has reshaped this earnings cycle: capital spending is no longer a footnote. It is the headline.

The Capex Curve Is Bending — Unevenly

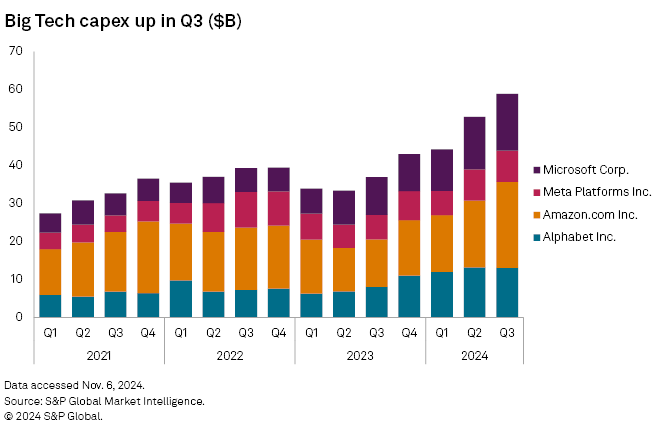

Across the four hyperscalers that reported in the past two weeks — Amazon, Alphabet, Microsoft, and Meta — aggregate 2026 AI-related capital expenditure commitments now exceed $725 billion, according to data compiled by MSN. Yet the market's reaction was anything but uniform. Alphabet shares jumped 9% in the session after its report, widening its year-to-date outperformance over the Nasdaq-100 to 14 percentage points. Microsoft and Meta, by contrast, sold off 6% and 8% respectively in post-earnings trading, erasing a combined $280 billion in market capitalisation over two days, per Peter Cohan's analysis in Forbes.

Investors are no longer writing blank cheques for AI ambition. They are rewarding proof of revenue accretion and punishing capex that lacks a visible return path.— Peter Cohan, Forbes, 30 April 2026

The divergence is not subtle. Alphabet's cloud segment grew 31% year over year, and the company was able to point to a direct line between its TPU v6 deployments and enterprise AI workload migration — revenue that showed up in the same quarter. Microsoft's Azure AI services also grew, at 33%, but its forward capex guidance of $95 billion for fiscal 2027, disclosed in the 10-Q filed 28 April, landed heavier because the accompanying revenue growth decelerated by two percentage points sequentially. The difference between these two reactions is not sentiment; it is free cash flow margin. Alphabet's operating margin expanded 180 basis points, while Microsoft's compressed 120 basis points on the same AI buildout. The market graded them on different curves.

Where the Money Goes — and Who Carries the Debt

Beneath the hyperscaler earnings lies an infrastructure layer that is absorbing capital at a velocity the public markets have not seen since the fibre buildout of 1999–2001. CoreWeave, the GPU-cloud operator that went public in March 2025, reaffirmed its $12 billion to $13 billion 2026 revenue outlook in its Q1 call and raised its 2026 exit run-rate floor to $18 billion as reported by Seeking Alpha. The company's contracted revenue backlog now approaches $100 billion, with Meta alone committing an additional $21 billion for capacity running through 2032. This is not a demand story; it is a financing story. CoreWeave's debt-to-equity ratio, adjusted for operating leases on its data-centre footprint, sits at 2.7x, and OpenAI — representing roughly a third of its contracted revenue — is itself burning approximately $4 billion a quarter, according to sell-side estimates from Morgan Stanley.

Capital spending crossed $725 billion this earnings cycle. The market rewarded exactly one hyperscaler for it.

The credit dimension is no longer peripheral. An analysis published by Investing.com on 9 May argues that the AI supercycle has become one of the largest debt-funded infrastructure expansions in corporate history, with the top four cloud operators and their supply chain issuing $190 billion in combined investment-grade bonds over the trailing twelve months. If the revenue does not materialise at the promised yield, the debt service does not pause. This is the constraint the equity market is beginning to price — not today's earnings beat, but the shape of the free-cash-flow line two years out, when interest expense on those bonds has compounded.

What Capital Allocation Reveals That Press Releases Do Not

Three patterns in the Q1 filings deserve more attention than they received on earnings calls. First, Amazon's capital lease additions — which bypass the capex line on the cash-flow statement but represent binding obligations — rose 44% year over year to $19.4 billion. Second, Microsoft's deferred revenue grew only 7%, the slowest rate since 2021, suggesting that large AI contracts are being signed but not yet booked as ratable revenue. Third, Meta's disclosure that inference workloads now account for 60% of its internal AI compute — up from 25% a year ago — implies a shift from training capex to serving opex, which changes the margin profile of its AI business in ways the company has not yet quantified. Taken together, these data points suggest the hyperscalers are entering a new phase of the cycle: the buildout is not complete, but the bill is coming due, and the revenue required to meet it is still largely in the forward-contract column.

- Amazon: TTM free cash flow fell from $26B to $1.2B; capital leases rose 44% to $19.4B in Q1.

- Alphabet: Cloud revenue +31%, operating margin +180 bps; stock outperformance of 14 pp vs. Nasdaq-100.

- Microsoft: Azure AI +33%, but forward capex of $95B for FY27 and decelerating revenue growth compressed margins.

- Meta: Inference now 60% of internal AI compute, shifting the cost structure from capex-heavy training toward opex-heavy serving.

- CoreWeave: $100B contracted backlog, $18B exit run-rate floor, but 2.7x adjusted leverage and concentrated customer risk in OpenAI.

The Morningstar analysis cited by CNBC on 8 May argues that tech stocks offer their best value in years after a succession of strong earnings seasons has allowed them to grow into their multiples. That may be true for the sector in aggregate. But the Q1 2026 cycle suggests investors are no longer treating all AI capex as equivalent. The premium is accruing to the companies that can show the revenue line moving in the same direction as the capital-expenditure line — and in the same quarter. My prediction, and it is only a prediction, is that the next two quarters will compress this divergence further: the hyperscalers that cannot map capex to cloud-revenue acceleration by Q3 2026 will find their cost of equity rising, not falling, even as headline earnings continue to beat.