China Cloud Growth Hits 26% in Q4, Third Straight Quarter Above 20%

While American hyperscalers command global headlines, China's cloud providers are reshaping Asia-Pacific markets through AI unbundling, chip substitution, and sovereign cloud architectures.

www.theregister.com

www.theregister.com

In this article

On April 29, 2026, research firm Omdia released a figure that landed quietly in the trade press: mainland China's cloud infrastructure services spending hit $14.7 billion in the fourth quarter of 2025, up 26 percent year-on-year. What made the number worth a second look was not the headline growth rate but the trajectory it confirmed. This was the third consecutive quarter in which China's cloud market expanded at above 20 percent, an acceleration pattern that had begun in mid-2025 and showed no sign of flagging. The figure did not come from one of the American hyperscalers that dominate the global rankings, but from a market where the competitive dynamics, regulatory architecture, and customer incentives all run on different rails. Readers who filed the report away as 'China doing well' missed the tell.

Context sharpens the signal. In that same Q4 2025 period, global enterprise cloud infrastructure spending crossed the $129 billion mark, according to Synergy Research Group data reported by CRN in early May 2026. China's $14.7 billion represented roughly 11 percent of the global total — a share that has been inching upward for two years. But the composition of that spend tells the real story. While American hyperscalers — AWS, Microsoft Azure, and Google Cloud — dominate global revenue on the back of broad enterprise adoption curves, China's cloud market is being shaped by three forces that do not map neatly onto Western assumptions: state-guided AI infrastructure buildout, a GPU-constrained supply chain forcing domestic substitution, and a growing sovereign-cloud instinct that is finding its first large-scale commercial expression in the Asia-Pacific region.

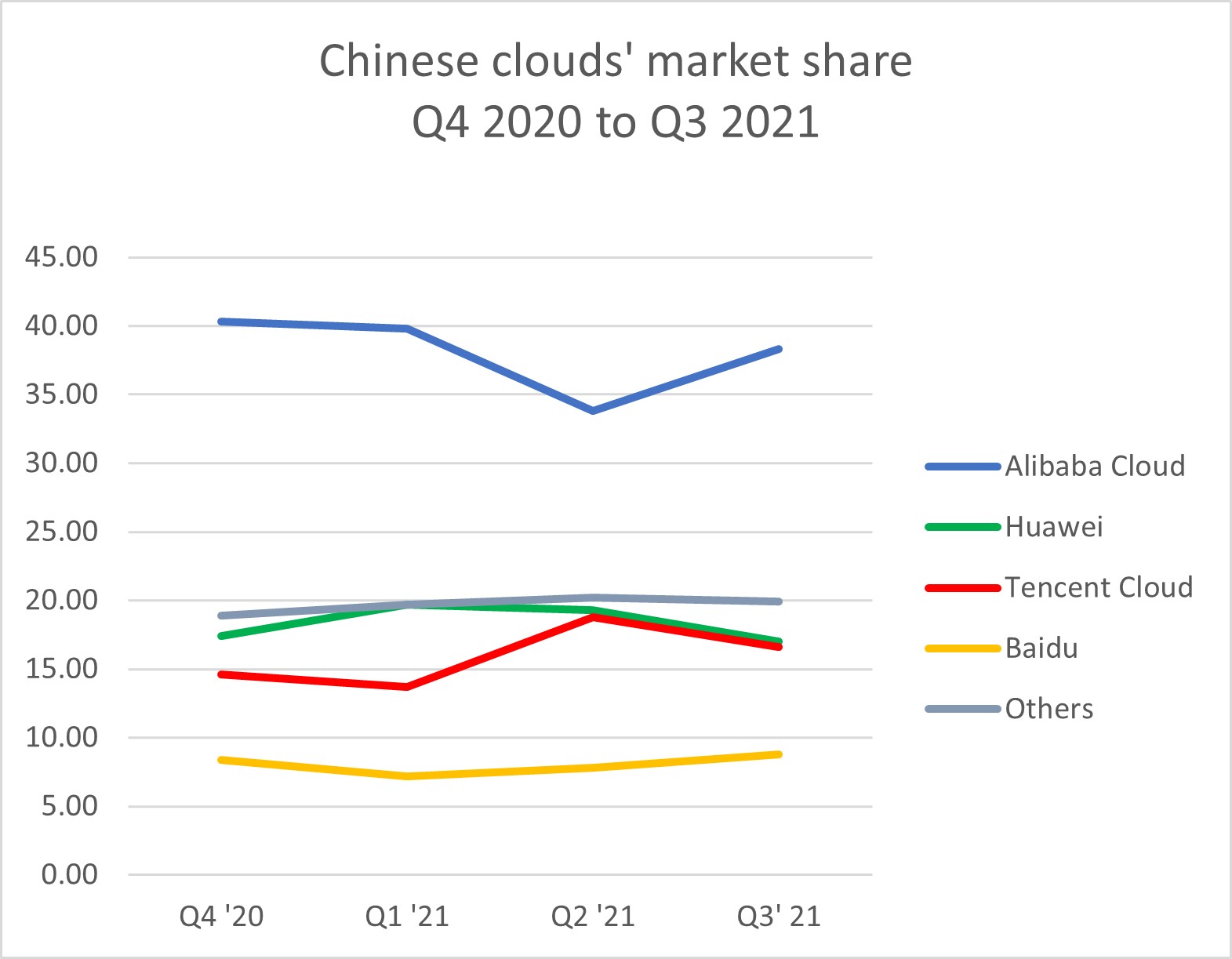

Alibaba Cloud remains the gravitational centre of the region. In late April 2026, Manila Standard reported that the unit held a 22.5 percent share of the Asia-Pacific IaaS market, making it the largest cloud provider by revenue in the region for another consecutive quarter. Globally, Synergy pegged Alibaba's IaaS market share at 7.7 percent, good for fourth place behind AWS, Microsoft, and Google. But there is a distinction worth preserving: Alibaba's cloud growth is increasingly AI-driven, and the company has begun unbundling that revenue. At its March 2026 quarterly report, Reuters noted that cloud revenue grew 36 percent year-on-year, and that Alibaba planned to separate its AI business from the cloud arm — an accounting move that signals management is treating AI workloads as a standalone growth line, not a feature of infrastructure.

That separation is the kind of quiet structural decision that rewards patience. For three quarters running, Alibaba executives have described AI-related revenue as accounting for more than 20 percent of the cloud unit's top line. Pulling it into a distinct entity does two things: it gives investors a clean line of sight into AI growth rates that would otherwise be obscured inside a $15 billion-plus cloud division, and it creates the organisational machinery to price, sell, and partner around AI services independently.

Tencent occupies a different lane, one that is harder for Western observers to benchmark. Its cloud division does not break out revenue with the granularity that Alibaba now provides, and the company has been selectively quiet about its infrastructure services ambitions in earnings calls. But the scale of the addressable base is not in question. With 1.4 billion users across Weixin/WeChat, Tencent sits on a distribution and data footprint that no Western hyperscaler can replicate inside China. In the past twelve months, the company has redirected its cloud strategy toward AI workloads that run closer to its consumer ecosystem — enterprise AI agents that plug into WeChat workflows, gaming infrastructure that doubles as GPU-as-a-service for third-party studios, and a financial-services cloud that draws on its WeChat Pay data environment. This is not infrastructure sold by the terabyte-hour; it is cloud capacity bundled with access to an ecosystem that Chinese enterprises cannot walk away from.

The Q1 market is now fifteen times larger than it was a decade ago and continues to expand at 35 percent annually. Reaching a half-trillion-dollar run rate underscores the far-reaching impact of cloud computing and AI on the IT landscape.— John Dinsdale, chief analyst at Synergy Research Group, in comments to CRN

Beneath the Alibaba-Tencent duopoly, a third structural shift is underway — one that concerns silicon more than software. In January 2026, the South China Morning Post reported that Baidu and Huawei Technologies collectively accounted for more than 70 percent of China's GPU cloud market, a segment that has become the bottleneck through which Chinese AI ambitions must pass. Huawei's Ascend processors and Baidu's Kunlun chips are not yet performance-competitive with Nvidia's latest-generation GPUs on raw benchmarks, but they are available — and availability, in a market hemmed in by US export controls, is a moat. Nvidia's share of the China AI chip market slipped to 55 percent by early 2026, according to a Barchart analysis, down from over 80 percent two years earlier. The remaining share is being captured by domestic alternatives that are improving their software stacks quarter by quarter.

The Sovereignty Fracture

If the China cloud market is being reshaped by chip supply chains and AI unbundling, the rest of Asia-Pacific — and increasingly Europe — is being reshaped by a parallel dynamic: the rise of the sovereign-first cloud procurement model. In an April 2026 analysis, SiliconANGLE documented how enterprises from banking to telecommunications are now defaulting to sovereign cloud architectures — infrastructure that guarantees data residency, local key management, and isolation from foreign jurisdictional reach — before they evaluate performance or cost. Google Cloud's announcement at its Next '26 conference of a Cloud Data Boundary that allows customers to keep data within prescribed geographic perimeters was greeted less as innovation than as table stakes. 'The cloud was supposed to simplify everything: global scale, shared infrastructure, one architecture for the world,' a Forbes Technology Council contributor wrote in March 2026. 'That model is shifting, and I don't see it shifting back again.'

The sovereign cloud conversation lands differently in Asia than it does in Europe. In the EU, sovereignty is primarily a regulatory construct — GDPR enforcement, the European Data Protection Board's rulings, and the cybersecurity certification schemes that Brussels has been refining since 2024. In Southeast Asia, sovereignty is more often a commercial and geopolitical calculation. Indonesia's government, through its national data centre programme, has mandated that certain categories of citizen data remain on infrastructure operated within the country. Thailand's Personal Data Protection Committee has begun issuing compliance orders that make cross-border data transfers more expensive by requiring impact assessments for each jurisdiction. Vietnam's forthcoming data law, expected to take effect in 2027, will require data localisation for a broad set of industries. None of these measures prohibits foreign cloud providers outright, but each raises the cost and complexity of operating a globally consistent cloud architecture — which is, in practice, what the hyperscalers sell.

The American cloud providers have responded, each in character. Microsoft's Azure Local, announced in late April 2026, now scales to thousands of nodes within a single sovereign deployment — a technical signal that the company expects these environments to run full production workloads, not just token edge instances. IBM, at its Think 2026 conference in early May, dedicated a substantial portion of its keynote to what it called an 'AI operating model' for sovereign environments, positioning its hybrid-cloud portfolio as the governance layer between public AI services and regulated data. AWS, characteristically, has said less in public but has been building out its Asia-Pacific region footprint at an accelerating pace, with a second Malaysian region and a dedicated Thailand Local Zone now operational. The unspoken assumption across all three: the era in which a Singapore or Tokyo region could serve the entire Asia-Pacific market is ending.

This fragmentation creates openings for the Chinese hyperscalers that did not exist five years ago. Alibaba Cloud now operates availability zones in Indonesia, the Philippines, Thailand, and Malaysia, and has been investing in local partner ecosystems — particularly in fintech and e-government — that give it political cover a US-flagged provider lacks.

Tencent, meanwhile, has been slower to build out international cloud availability but faster to invest in the AI platforms that make those buildouts stickier. Its April 2026 discussions with DeepSeek — the Hangzhou-based AI startup seeking a valuation above $20 billion, as reported by MSN — are the third such investment signal in a year. Both Alibaba and Tencent are reportedly participating, positioning themselves not merely as cloud vendors but as equity stakeholders in the models that will consume the most compute. For a regional enterprise evaluating cloud providers, that distinction matters: a cloud contract with Alibaba or Tencent increasingly comes with preferential access to model capacity that AWS and Google Cloud cannot yet offer in their Asia-Pacific regions.

There is a danger in reading too much of a unified 'China cloud strategy' into these moves. Alibaba, Tencent, Huawei, and Baidu compete with one another as aggressively as they compete with American rivals — and in the GPU cloud market, arguably more so. The SCMP's finding that Huawei and Baidu control 70 percent of China's GPU cloud market means that Alibaba and Tencent, for all their scale, are not the primary beneficiaries of the domestic chip-substitution trend. That forces both companies to differentiate on software and platform stickiness rather than on raw compute supply — a dynamic that, if sustained, could produce a cloud market that looks less like the American model of infrastructure-led dominance and more like a services-and-ecosystem oligopoly.

What to Watch in Q3

Three indicators will determine whether the regional dynamics described here harden into durable structural change or fade into a cycle. The first is Alibaba's AI revenue disclosure: if the separated AI unit reports a growth rate above 40 percent in its first standalone quarter, the market should treat that as confirmation that AI workloads are pulling away from general-purpose cloud growth — a signal that would accelerate investment in regional AI capacity. The second is Huawei's Ascend chip yield data: any public disclosure, however oblique, that domestic GPU production is scaling to meet AI training demand would reshape the competitive arithmetic for every cloud provider operating in China. The third is the first major Southeast Asian government contract awarded under explicit sovereign-cloud criteria: Thailand's digital government procurement round, expected in the third quarter, is the one to watch. Which cloud provider wins, and on what terms, will be a better indicator of regional intent than any analyst forecast.

John Dinsdale's half-trillion-dollar run rate is not a ceiling. If the current trajectory holds, Synergy will be reporting a $600 billion annualised market before the end of 2027. But that growth will not be evenly distributed — not by provider, not by region, and not by architecture. The cloud market that was supposed to be flat and global is developing borders, and those borders are being drawn not in data centres but in procurement policies, chip export licences, and the quiet margins of earnings calls. The question for the next two quarters is not who is winning but which map they are playing on.

Read next