HSR Vacatur Stands: Premerger Filing Clock Resets After Fifth Circuit

With the FTC's 2024 Hart-Scott-Rodino rule overhaul vacated and the premerger filing clock reset, agencies are now seeking public input on a new notification regime, leaving dealmakers in a state of cost relief mixed with regulatory uncertainty.

www.stinson.com

www.stinson.com

In this article

On March 19, 2026, the U.S. Court of Appeals for the Fifth Circuit denied the Federal Trade Commission's motion to stay a district court ruling that had vacated the agency's October 2024 overhaul of the Hart-Scott-Rodino premerger notification rules. The one-page order, entered in Chamber of Commerce of the United States v. FTC, No. 24-40682, ended a month of whiplash in which the new, expanded HSR form had been invalidated, temporarily revived by an administrative stay, and then invalidated again. For the first time in more than a year, merging parties were directed to file using the pre-2024 notification form, the shorter and far less burdensome document that had governed HSR practice since 1978.

Six days after the Fifth Circuit's ruling, on March 25, the DOJ Antitrust Division and the FTC issued a joint Request for Information seeking public comment on the future of premerger notification. The RFI, published in the Federal Register, asked a series of open-ended questions about what information the agencies should require from merging parties, how far back prior-acquisition disclosures should reach, and whether certain categories of transactions should be exempt. The comment period signaled that the agencies, rather than appealing the Fifth Circuit's decision further, might instead pursue a new rulemaking calibrated to survive judicial review. As Wiley Rein attorneys noted in a client alert on the RFI, the agencies are treating the vacatur less as the end of expanded HSR requirements than as a procedural reset.

The rule the courts struck down had been the most significant revision to the HSR premerger notification regime since the statute was enacted in 1976. Adopted by the FTC in a 3-2 vote in October 2024, the Final Rule required filers to submit draft transaction agreements, narrative descriptions of competitive overlaps, organizational charts, details on supply relationships, prior-acquisition histories stretching back a decade, and information on labor-market classifications and foreign subsidies. Law firms estimated that the new form could take 200 to 400 hours to complete for a complex transaction, compared to roughly 40 to 80 hours under the old form. The U.S. Chamber of Commerce, the Business Roundtable, and other trade associations sued, arguing that the FTC had exceeded its statutory authority under the Administrative Procedure Act and imposed compliance costs that bore no reasonable relationship to the statutory purpose of screening transactions for competitive harm.

Judge Amos L. Mazzant III of the Eastern District of Texas agreed. In a February 12, 2026 order, he vacated the Final Rule in its entirety, finding that the FTC had failed to adequately consider the costs of its expanded information demands and had not provided a reasoned basis for departing from decades of settled practice. The ruling, analyzed in detail by Hughes Hubbard & Reed, left the agencies with the option of appealing to the Fifth Circuit or returning to the drawing board. The FTC chose to appeal and sought a stay pending appeal. The Fifth Circuit briefly granted an administrative stay on February 19, then reversed course on March 19, denying the stay in a brief order that left the district court's vacatur fully operative.

The practical effect of the vacatur was immediate and sweeping. Akerman LLP, in a client advisory published after the Fifth Circuit's decision, noted that the reversion to the old HSR form materially reduced filing burdens for reportable transactions. Parties that had begun preparing submissions under the expanded requirements could abandon work on draft agreements, narrative competitive analyses, and organizational disclosures that the old form never required. For transactions that had been filed under the new rules during the brief window when they were operative, it was unclear whether those filings would need to be resubmitted using the old form, though the agencies did not immediately require refiling.

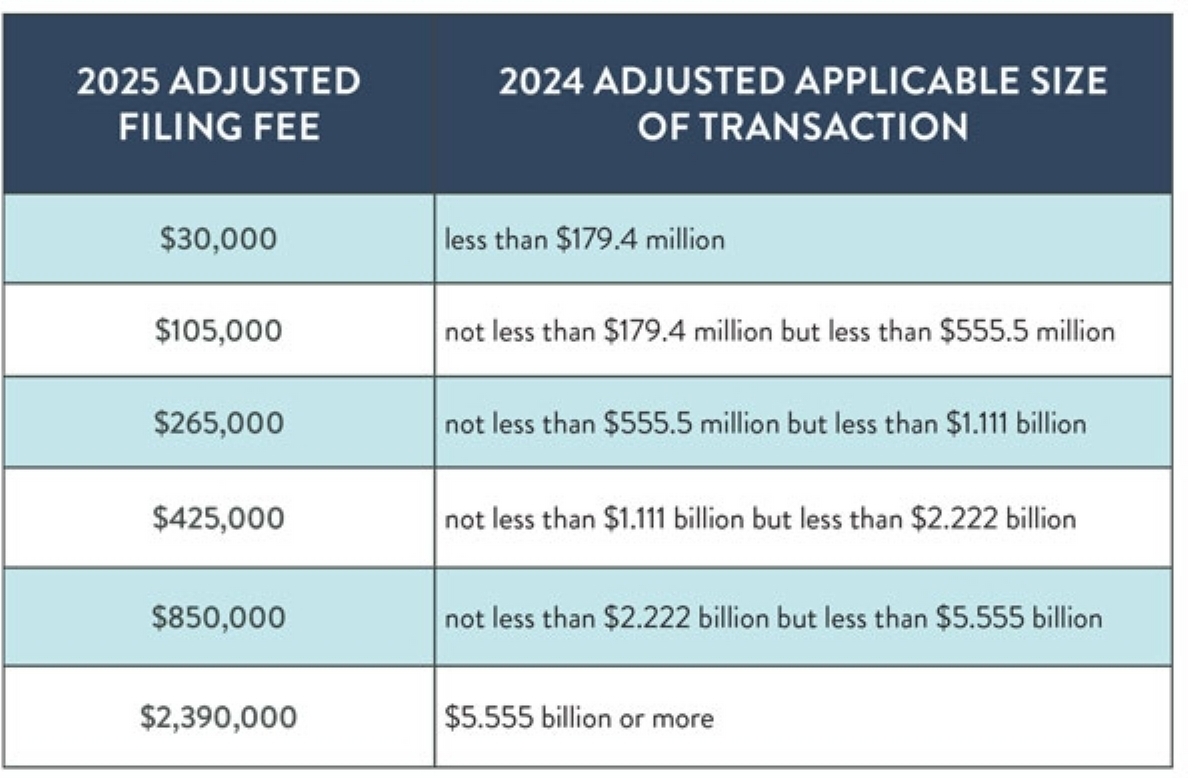

The compliance whiplash was especially acute for law firms and in-house deal teams that had spent much of 2025 building internal protocols around the expanded HSR form. Whiteford Taylor & Preston, in a client alert dated March 31, walked through the return of the old form in detail, noting that the pre-2024 notification required only a relatively modest set of documents: the transaction agreement, certain Securities and Exchange Commission filings, financial statements, and revenue data by industry code. The firm advised clients that the old thresholds remained in place, with the size-of-transaction test standing at $133.9 million for 2026, and that transactions below that threshold, or those qualifying for an exemption, remained non-reportable.

The March 25 RFI, however, made clear that the old form may not be the old form for long. The agencies asked whether they should require labor-market information, details on supply-chain relationships, information about foreign subsidies, and narrative descriptions of the strategic rationale for a transaction. These are precisely the categories of information that the vacated 2024 rule had demanded, and their inclusion in the RFI suggested that the agencies intend to reintroduce many of the same requirements through a new rulemaking that might better withstand APA scrutiny. The comment deadline was set for late May 2026, and a broad coalition of business groups, antitrust practitioners, and academic commentators were expected to weigh in.

The rulemaking uncertainty unfolded against a backdrop of increasing HSR filing volume. According to White & Case's Global Antitrust Merger StatPak, HSR filings in the first quarter of 2026 increased 14 percent over the same period in 2025, a continuation of a steady upward trend that began in late 2024. The increase reflected both robust M&A activity and the fact that the old form, for all its deficiencies in the agencies' view, imposed a lighter compliance cost than the vacated rules. Some antitrust practitioners suggested that certain transactions that had been delayed during the period of regulatory uncertainty were now moving forward under the familiar, less demanding notification regime.

The deal-flow data bore this out. On April 24, the Joplin Globe reported that Merck announced the expiration of the HSR waiting period for its acquisition of Terns Pharmaceuticals, clearing the antitrust portion of the regulatory path. A day earlier, the Rutland Herald reported that RB Global announced early termination of the HSR waiting period for its BigIron acquisition. The early termination, granted on April 21, signaled that the agencies had concluded their review without identifying competitive concerns, a process made faster by the return to the old form's streamlined document demands. Similar announcements from SiTime and SunOpta in the same period underscored the return to a more predictable, if provisional, notification calendar.

The agencies, meanwhile, were signaling that they would not retreat from aggressive merger enforcement even as their procedural tool was being rebuilt. On May 7, Acting Assistant Attorney General Omeed A. Assefi delivered remarks at NYU Law's Engelberg Center on innovation and antitrust, a speech analyzed in depth by Axinn, Veltrop & Harkrider. Assefi outlined the Antitrust Division's current approach to merger review, emphasizing continuity with the prior administration's enforcement posture. The Axinn analysis noted that Assefi's remarks were notable for what they did not say: there was no announcement of a wholesale retreat from structural presumptions, no signal that the Division would back away from challenging vertical mergers or transactions in technology markets.

The same speech drew coverage from Reuters, where Jody Godoy reported that Assefi warned companies against attempting to mislead antitrust reviewers about the role of artificial intelligence in their businesses. The warning, delivered in the context of merger review, reflected a concern that dealmakers might characterize AI capabilities in ways designed to either minimize competitive overlaps or exaggerate efficiencies. Assefi's remarks, as summarized by both Axinn and Reuters, positioned the Division as attentive to the ways in which AI-related claims could distort the merger review process.

What to Watch for Next

Several parallel developments will shape the HSR landscape in the months ahead. First, the FTC and DOJ are considering whether to eliminate longstanding exemptions that shield most real estate transactions from HSR reporting requirements. A separate rulemaking proceeding, with a comment deadline of May 26, has signaled that the agencies view the real estate exemption as an unjustified gap in their merger screening authority. If the exemption is narrowed or removed, a significant new category of transactions would become reportable, adding volume to an HSR calendar that is already seeing double-digit year-over-year growth.

Second, Congress is paying attention to transactions that are structured specifically to avoid HSR review. On March 19, Senators Elizabeth Warren and Richard Blumenthal sent a letter to NVIDIA CEO Jensen Huang questioning whether certain of the company's transactions had been designed to fall below the HSR thresholds while still conferring competitive advantages. The letter, covered by a JD Supra analysis, raised the prospect that legislative action could follow if the agencies prove unable to address HSR avoidance through regulation alone. Any congressional intervention would add another layer of unpredictability to a process that has already seen its governing rule vacated, then revived, then vacated again within a single quarter.

Third, the broader appellate posture of the 2024 rule remains unresolved. The Fifth Circuit's denial of a stay pending appeal did not dispose of the underlying appeal itself. The FTC could still pursue a full merits appeal, though the March 25 RFI suggested that the agencies might prefer a new rulemaking to the risk of an adverse appellate ruling that would constrain their authority more permanently. Antitrust practitioners are watching the docket in Chamber of Commerce v. FTC for any indication of whether the government will continue to litigate the validity of the 2024 rule or instead dismiss the appeal and focus entirely on the new rulemaking.

For now, the HSR calendar operates on borrowed time. The old form governs, but the agencies have made clear they believe it is inadequate. The RFI process will produce a record that could support a new rule as early as late 2026 or early 2027. Dealmakers who are closing transactions today under the pre-2024 requirements should understand that they are working in an interregnum. The question is not whether expanded HSR requirements will return, but what form they will take, how much they will cost to comply with, and whether the next Final Rule can survive the judicial scrutiny that the last one could not.

Read next