Retail Capital Reshapes Venture Fund Formation, LPs Take Notes

Robinhood's publicly traded venture fund now holds OpenAI shares, and AngelList's regulated VC fund accepts a $500 minimum, together tapping billions from retail investors who have never encountered a capital call.

dealroom.net

dealroom.net

In this article

On April 17, 2026, Robinhood Ventures Fund I purchased approximately $75 million of OpenAI Series A Preferred Stock in a primary transaction, the company announced via Globe Newswire. The buyer was not a Sand Hill Road partnership with a $2 billion fund and a 2-and-20 fee structure. It was a publicly traded closed-end fund listed on the New York Stock Exchange under the ticker RVI, a vehicle designed to let retail investors buy exposure to private technology companies the same way they buy shares of an ETF. The purchase brings RVI's portfolio alongside earlier positions in Stripe, ElevenLabs, Databricks, and Revolut. For the venture fund formation cycle, the trade marks something larger than another AI allocation: it signals that the capital base for venture is being rewired from the bottom up.

The rewiring is happening at speed. In the last two months of spring 2026 alone, three structurally distinct retail-access venture products either launched, scaled, or made their first headline allocations. RVI, which began trading in March, attracted more than 150,000 retail investors, Robinhood CEO Vlad Tenev told TechCrunch. AngelList, the platform that pioneered online syndication, launched USVC, a registered fund with a $500 minimum investment that provides access to private companies for accredited and non-accredited investors alike, Crowdfund Insider reported. Meanwhile, Robinhood's earlier deals, including a $14.6 million Stripe purchase and a nearly $20 million ElevenLabs Series D position, were disclosed in March filings covered by Seeking Alpha. Three different structures, one shared thesis: the institutional LP model is leaving too much capital, and too much access, on the table.

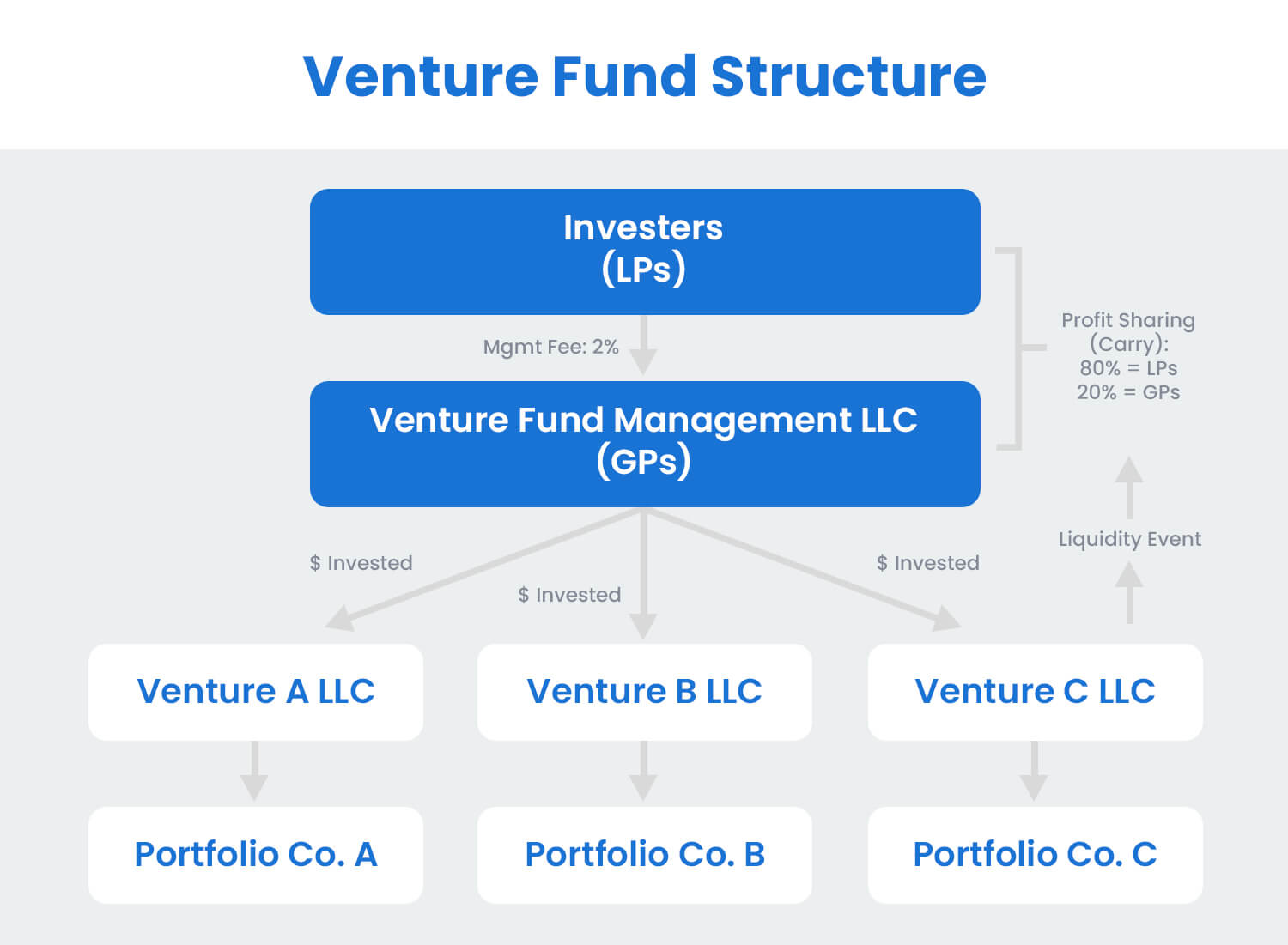

The traditional venture fund formation cycle is built on a premise that has not changed meaningfully in four decades. A general partner, or a small team of them, raises a 10-year blind pool from a concentrated group of institutional limited partners, typically endowments, foundations, pension funds, and fund-of-funds. Those LPs commit capital in increments of $5 million to $50 million, receive quarterly reports, attend annual meetings, and have no liquidity until distribution events that may arrive in year seven or never. The GP charges 2 percent management fees and 20 percent carried interest on profits above a hurdle. That structure worked when venture was small, when fund sizes rarely crossed $500 million, and when the number of funds raising in any given year was measured in the low hundreds. None of those conditions holds in 2026.

Jay Rogers, a 30-year veteran of private markets who worked at Morgan Stanley and Bear Stearns before managing funds and advising family offices, put the diagnosis plainly in a RealClearMarkets essay this month. The venture capital industry, Rogers argued, has become a system in which 'the GPs have all the control and the LPs have all the risk.' The lockup is too long, the information asymmetry too wide, the fee load too heavy relative to the public-market alternatives that now exist. What is changing, Rogers wrote, is that public markets are building mechanisms to replicate venture exposure with daily liquidity and transparent pricing, mechanisms that do not require a family office to trust a GP's DPI number from a pitch deck.

For emerging managers trying to raise their first or second institutional fund, the LP environment has tightened to a degree that makes 2021 look like a different geological epoch. A Forbes analysis by Ilona Limonta-Volkova noted that LP patience is thinner, deployment timelines are under heavier scrutiny, and capital is gravitating toward the largest established managers. Solo GPs, the piece argued, are surviving only if they can demonstrate genuine sourcing edge, operational value to founders, and a concentrated portfolio thesis that does not look like a beta play on SaaS. The tourists, Limonta-Volkova wrote, have left the building. What remains is a smaller cohort of GPs whose personal conviction, rather than a diversified team or a brand, is the product LPs are being asked to underwrite.

That filtering shows up in the rebranding and restructuring moves rippling through the seed and early-stage ecosystem. In April, the Portland-based Cascade Seed Fund rebranded to Long Way Ventures as it prepared to raise its next fund, the Business Journals reported. A rebrand alongside a new fundraise often signals a strategy reset, a fund-size recalibration, or an attempt to distance a fresh vehicle from a prior vintage whose IRRs are still legible to LPs running diligence. In the current market, any of those explanations is plausible. The name change, from a regional natural-feature moniker to a phrase that implies patience and distance, is its own kind of signal: LPs are being asked to take the long way, and the GP is branding around that ask.

Not every fund formation story in 2026 is a story of constraint. Level Equity Management closed its third structured capital fund at $2 billion in March, according to a PR Newswire release. The vehicle sits between growth equity and credit, offering expansion capital to middle-market technology companies. The size of the close, and the fact that it was a structured capital fund rather than a pure equity vehicle, suggests that LPs remain willing to write large checks when the risk-return profile reads as something other than '10-year blind pool for software startups at 50x revenue multiples.' Structured capital offers downside protection, contractual returns, and shorter duration, the exact features that the Rogers critique says traditional venture lacks.

The structural innovation that RVI and USVC represent operates on a different axis entirely. They are not competing with Level Equity for institutional commitments. They are competing with the idea that venture access should require an introduction to a GP. RVI is a '40 Act fund, which means it registers under the Investment Company Act of 1940, files quarterly holdings reports, and trades on an exchange with daily liquidity. Investors buy and sell shares through a brokerage account. The fund itself holds private company stock, but the wrapper is public-market plumbing. USVC, AngelList's product, takes a different approach: a registered, non-traded fund that lowers the minimum to $500, targeting the retail investor who would never meet an accredited-investor threshold, let alone get a capital-call notice from a traditional venture partnership.

After 30 years in private markets, including work at Morgan Stanley and Bear Stearns, and later managing funds and advising family offices, I've come to a conclusion the venture capital industry doesn't want to hear: the market is fixing what GPs refused to fix themselves., Jay Rogers, writing in RealClearMarkets, May 2026

The Rogers argument is that venture's structural defects, the opacity, the 10-year lockup, the J-curve that penalizes LPs for the first half-decade, the recycling of management fees into new funds before the old ones have distributed, are not features of the asset class. They are features of a power imbalance. When capital was scarce and venture was an obscure corner of the alternatives universe, GPs could dictate terms. Now that platforms like Robinhood and AngelList have built regulated, liquid, low-minimum products, the imbalance is starting to correct, not through LP negotiation but through product substitution.

The implications for fund formation in 2027 and 2028 are significant. If retail-access vehicles can aggregate billions of dollars, and RVI's $75 million OpenAI check alongside its Stripe, ElevenLabs, and Databricks positions suggests they can, then the largest late-stage private companies may begin to prefer these vehicles as a capital source. A retail fund that buys Series A Preferred Stock and holds it in a transparent, exchange-traded wrapper does not demand a board seat, does not push for governance changes, and does not call the founder at 10 p.m. asking about the burn rate. The check clears, the allocation is disclosed quarterly, and the fund's own investors manage their exposure through their brokerage app.

The traditional GP response to this thesis is that retail capital is dumb capital. It does not bring portfolio support, hiring networks, customer introductions, or follow-on reserves. It cannot help a company navigate a down round or a restructuring. These are real objections, and they explain why the seed and Series A segments, where company-building assistance still matters, are unlikely to be disrupted by the retail-wrapper model in the near term. But at Series D and later, where check size and price matter more than board composition, the objection weakens. RVI's portfolio of Stripe, OpenAI, ElevenLabs, Databricks, and Revolut reads like a growth-stage fund that happens to be listed on the NYSE.

There is also a market signal embedded in RVI's first months of trading, and it is not an uncomplicatedly bullish one. The fund fell 11 percent on its first day of trading on March 6, CNBC reported. A publicly traded closed-end fund can trade at a discount or premium to its net asset value, and RVI's early discount suggested that retail investors were not yet convinced the underlying portfolio was worth the listed price, or that they understood the vehicle's structure well enough to price it. The discount has implications for the fund's ability to raise additional capital through secondary offerings, and for the broader thesis that retail demand for venture exposure is deep and durable.

For fund managers in the middle, those raising $50 million to $250 million vehicles from institutional LPs, the retail-access trend adds a new dimension to an already difficult fundraising environment. They are now competing not only with other GPs for LP attention but with products that offer the LP's own beneficiaries a simpler, cheaper, and more liquid path to venture exposure. A university endowment that commits $25 million to a traditional venture fund is making a 10-year illiquid bet with high fees. That same endowment could, in theory, allocate a portion of its venture bucket to a publicly traded vehicle and mark it daily. The fiduciaries will notice.

What the Marketing Tells Us About the LP Funnel

One consequence of the tighter LP market is that fund managers are being forced to build public-facing brands, a shift that would have seemed undignified to the partnership class of 2015. A Forbes analysis by Josipa Majic this April argued that emerging managers who market with specificity, transparency, and a willingness to build in public are winning more deals than those relying on closed-network introductions. The thesis is that founders, who are themselves increasingly sophisticated about fund structures, track records, and LP quality, now treat a GP's public presence as a diligence signal. A fund that cannot articulate its edge in public, the reasoning goes, may not have one.

This dynamic loops back to the retail-access trend in an interesting way. The skills required to market a fund to institutional LPs are distinct from the skills required to market one to 150,000 retail investors, but they are converging around a common demand for transparency. The institutional LP wants to see the track record, the deal memos, the reference calls. The retail investor wants to see the holdings, the expense ratio, the daily price. Both are asking, in different registers, for the same thing: show me what I am buying, and tell me what it costs. The traditional venture model, with its capital calls, its recycling, its net-IRR figures that blur the line between realized and unrealized returns, was not designed to answer that question clearly.

The State of Venture Capital in 2026 report from TrueBridge Capital, the data partner behind the Forbes Midas List, framed the year as the start of a 'value creation era' in which AI dominance, selective capital allocation, and a slowly recovering IPO window are reshaping how funds deploy and how LPs assess performance. Median pre-money valuations increased across stages, the report noted, which means funds are writing larger checks for the same ownership stakes. That math only works if exit values rise proportionally, which places enormous pressure on the few companies that actually go public or get acquired at scale. In that environment, the fund that can show mark-to-market pricing every day, rather than once a quarter with a three-month lag, has a structural advantage in managing LP expectations.

The next 18 months will test whether the retail-access model is a complement to traditional fund formation or a substitute for it. RVI's portfolio construction, concentrated in the most liquid and widely held private names, suggests a complement: the fund is buying stakes that traditional venture funds already own, effectively providing a secondary liquidity path. USVC, with its $500 minimum and broad mandate, is closer to a substitute, offering direct exposure to private companies through a regulated fund structure that bypasses the GP entirely. If both models scale, the traditional LP will have a new question to answer at every re-up meeting: why am I paying 2-and-20 for a product I can buy in my brokerage account?

Cascade Seed Fund's decision to become Long Way Ventures is, in this light, either a smart repositioning or an acknowledgment of an uncomfortable structural reality. The 'long way' is the traditional venture path: raise from institutions, deploy over three years, support portfolio companies through multiple financing rounds, and wait for exits that may take a decade. The new way, the Robinhood-AngelList way, is shorter, more transparent, and already has 150,000 investors who have never heard the term 'capital call.' The market is not waiting for the GP community to decide which model wins. It is pricing both, every day, on screens that anyone with a phone can see.

Read next