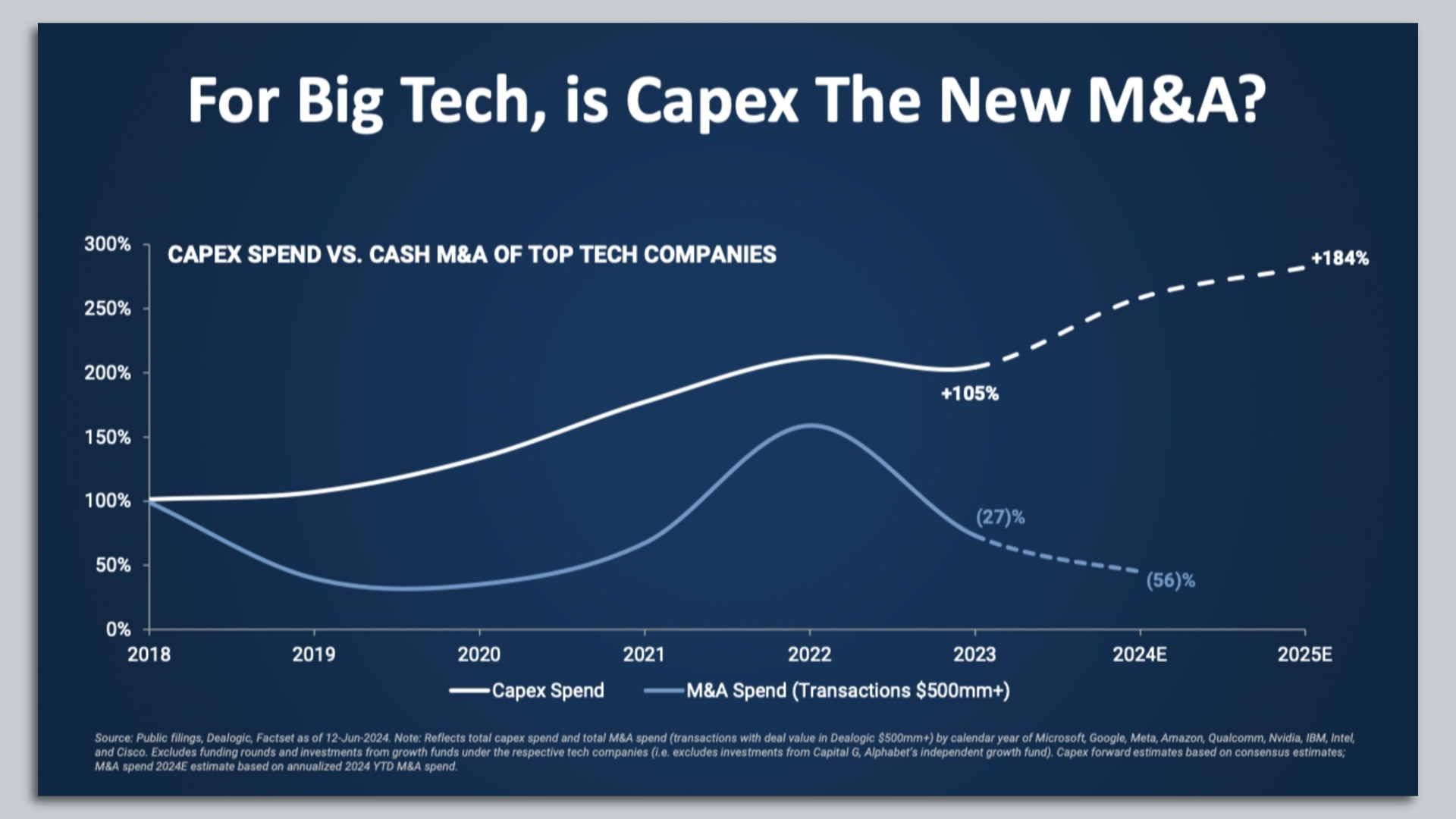

Big Tech's $750 Billion AI Capex Redraws the Earnings Cycle

Alphabet, Amazon, Meta, and Microsoft, the four hyperscalers, reported Q1 earnings that point to a collective capex of nearly $750 billion, yet the market reaction split sharply, revealing a deep tension between growth investment and free cash flow.

axios.com

axios.com

In this article

When Alphabet lifted its full-year 2026 capital expenditure guidance to as much as $190 billion on April 29, the number registered less as a surprise and more as a confirmation. The company had just reported first-quarter revenue of $109.9 billion, up 20 percent year over year, driven by a 63 percent surge in Google Cloud sales. The cloud backlog, a forward indicator of contracted but unrecognized revenue, had swelled to roughly $462 billion. And yet the line item that dominated the earnings call and the analyst notes that followed was not revenue or backlog. It was the word significantly, the adverb Alphabet's chief executive used to describe the expected increase in capex for 2027.

That single word, delivered in the cautious cadence of a prepared earnings script, crystallized what has become the defining tension of the 2026 earnings cycle. Across the four hyperscalers, Alphabet, Amazon, Meta, and Microsoft, combined capital expenditure is on pace to reach between $725 billion and $750 billion this year, according to estimates compiled by Forbes and Statista. That figure, which would have strained credulity two years ago, now arrives with the routine predictability of a quarterly 10-Q. The question is no longer whether the spending will happen. The question is what it buys, at what cost, and for whom.

The first-quarter earnings stretch that concluded in early May produced a market reaction that was far from uniform. Alphabet shares surged on the back of cloud momentum and a 130 percent 12-month return. Amazon held its $200 billion capex target for 2026 without rattling investors, even as Yahoo Finance reported that the company's free cash flow had collapsed from $26 billion to $1.2 billion. Microsoft posted 18 percent revenue growth and saw its Azure unit accelerate, yet heavy infrastructure spending renewed questions about the long-term margin profile of the intelligent cloud business. The starkest divergence, however, belonged to Meta.

Meta delivered first-quarter revenue of $56.3 billion, beating Wall Street estimates. The company raised its 2026 capex forecast to as much as $145 billion, citing underestimated compute needs and rising component costs. The stock tumbled roughly 6 percent. Insider characterized the investor reaction as a penalty for spending that outpaced even the upgraded consensus. The market had drawn a line: cloud revenue that demonstrably converts AI infrastructure into contracted backlog earns the benefit of the doubt. Platform advertising revenue, no matter how strong, does not command the same indulgence when paired with a nine-figure capex revision.

What makes this moment structurally unusual is that the earnings themselves, the top-line and bottom-line numbers, were broadly strong. The four hyperscalers collectively grew revenue at double-digit rates. Operating margins, outside of the depreciation charges that the capex build will eventually pull through the income statement, held or improved. Cloud businesses accelerated. AI services crossed from experimental line items into material revenue contributors. In any conventional earnings cycle, these results would have been unambiguously positive. The unease is not about the quarter that was. It is about the quarter that capital allocation implies is coming.

The Macro Divide Beneath the Micro Numbers

Running beneath the firm-level earnings analysis is a macroeconomic debate that has become unusually explicit among prominent technology investors. On a recent episode of the All-In Podcast featuring guest Gavin Baker, the roundtable examined the same dataset, Treasury yields, sovereign debt trajectories, AI infrastructure build rates, energy capacity, and arrived at investment outlooks that could not have been more opposed. As AOL reported, David Friedberg laid out a thesis organized around a building global bond crisis and a sovereign debt spiral. Baker, the founder of Atreides Management, argued the opposite side: that American energy independence and the productivity gains embedded in the AI factory buildout would overwhelm the fiscal headwinds.

That divide is not merely an intellectual exercise conducted on a podcast. It maps directly onto the earnings-season dispersion. The bearish macro case, rising real rates, compressed equity risk premiums, a buyer's strike on duration assets, would punish the companies that are borrowing the most to fund the longest-dated infrastructure assets. The bullish case, an AI-driven productivity upcycle that lifts trend GDP growth and validates current multiples, requires the capex to convert into revenue on a timeline that the bond market is not yet pricing. Each quarterly filing either supplies evidence for one side or the other, and the May 2026 earnings stretch supplied evidence for both.

Consider the capital structure implications. The four hyperscalers are not funding $750 billion in annual capex entirely from operating cash flow. Debt issuance has accelerated. Cash reserves are being drawn down. Depreciation schedules are lengthening as server and networking equipment useful lives are extended, a perfectly legal accounting choice that flatters near-term earnings but defers the recognition of the very costs the capex represents. MarketWatch quoted an analyst who described the spending as the "greatest capital misallocation in history," a phrase that has ricocheted through investor forums precisely because it names the fear that the bull case is built to suppress.

The Dormant Giants and the Supply Chain Signal

Not every company in the AI capex complex is a hyperscaler. 24/7 Wall St. flagged two enterprise technology giants, IBM and Oracle, that have quietly compounded earnings and built backlogs largely invisible to the retail investor conversation that has been trained on NVIDIA, Microsoft, and Meta. Oracle, in particular, has accumulated a cloud infrastructure backlog that, while smaller in absolute terms than the hyperscalers', has grown at a rate that implies enterprise customers are building multi-cloud redundancy into their AI procurement strategies. If the hyperscaler capex is the headline, the dormant giants represent the footnotes that occasionally rewrite the article.

The supply chain is telling a complementary story. The Star reported from Kuala Lumpur that Malaysian semiconductor stocks, particularly automated test equipment players, are riding an AI-driven upcycle that shows little evidence of peaking. Companies such as ViTrox and Unisem have seen order books lengthen into 2027, a detail that matters because ATE is a late-cycle indicator. Test equipment orders rise after fabrication capacity is installed and before end devices ship. That the ATE cycle is still accelerating suggests the capex cycle has further to run, and that the depreciation charges now beginning to appear on hyperscaler income statements represent only the earliest tranche of the spending that has already been committed.

The capital expenditure rankings, as compiled by Fast Company following the earnings reports, place Amazon at the top at $200 billion, followed by Microsoft and Alphabet in the $185 billion to $190 billion range, and Meta at $140 billion to $145 billion. Apple, notably, sits at a fraction of those figures, its AI strategy relying on on-device inference and a capital-light model that looks increasingly idiosyncratic. The gap between Apple and the other four has become a useful control group for the question of whether the hyperscaler spending is necessity or choice. So far, Apple's relative underperformance in AI services suggests it is necessity.

The market has been really sanguine about negative free cash flow. At some point, the bill comes due., A caller on Bloomberg Businessweek's Big Tech Special earnings panel, as reported by Yahoo Finance

The sanguinity that the Bloomberg caller identified is measurable. Amazon's free cash flow fell from $26 billion to $1.2 billion in a single quarter, a decline of roughly 95 percent, and the stock's reaction was a shrug. Alphabet's free cash flow, while healthier, is being diverted at an accelerating rate toward data center construction and custom silicon. Meta's capex-to-revenue ratio has crossed thresholds that, in any prior cycle, would have triggered a far more severe market reaction. The market's forbearance is itself a data point. It reflects a consensus that the AI infrastructure build is not discretionary, that failing to spend is strategically riskier than spending and being wrong.

That consensus, however, rests on assumptions about the revenue conversion rate that remain unproven at scale. Google Cloud's 63 percent growth is impressive, but it starts from a base that was, until recently, a distant third in the cloud market. AWS grew 28 percent, a rate that is healthy by the standards of a $100 billion-plus revenue run rate but does not, on its own, justify the $200 billion in capex that Amazon is deploying. Microsoft's Azure growth was strong but decelerating at the margin. The revenue is real. The question is whether it is sufficient.

There is a second, subtler question embedded in the capex figures: how much of the spending is defensive. When Alphabet says it expects to significantly increase capex in 2027, it is not merely forecasting its own ambitions. It is signaling an expectation that its competitors will do the same, and that the cost of not matching them, in cloud market share, in AI model capability, in enterprise lock-in, exceeds the cost of the spending itself. The capex numbers have become, in effect, a form of mutually assured construction. Each hyperscaler is building as though the others will not stop, because the evidence of the last eight quarters is that they will not.

The macro dimension compounds the uncertainty. If Friedberg's debt-spiral thesis is correct, the cost of capital that the hyperscalers face when they roll their debt, or issue new debt to fund the 2027 increment, will be higher than it is today. A 100-basis-point increase in the weighted average cost of debt for the four hyperscalers would add tens of billions of dollars to annual interest expense over the next five years. That is a manageable headwind if AI revenue grows at the pace the companies are projecting. It becomes a problem if the revenue curve bends.

Conversely, if Baker's AI-factory thesis proves out, the hyperscalers are not overspending but underinvesting relative to the addressable market that will exist in 2028 and 2029. The debate cannot be settled by a single quarter's earnings. But the earnings do provide a framework for tracking which side of the argument is gaining evidentiary support. On that score, the first quarter of 2026 was a draw: cloud revenue accelerated, margins held, but free cash flow evaporated and the capex guidance for 2027 tilted further upward. A draw, in a market that has priced in a decisive victory for the AI bulls, is not neutral.

What to watch next is not the topline revenue numbers, which have been strong enough to keep the narrative intact, but three less obvious indicators. The first is the cloud backlog-to-capex ratio: are the contracted future revenues growing faster than the investment required to serve them? The second is the depreciation schedule: will any of the hyperscalers reverse the useful-life extensions that have been flattering margins, and if so, on whose earnings call will that reversal first appear? The third is the debt markets: spreads on hyperscaler paper remain tight, but they are a real-time referendum on the creditworthiness of the AI buildout. The day those spreads widen, the earnings-cycle conversation will shift from the P&L to the balance sheet. That shift, when it comes, will be the signal that the great macro divide of 2026 has been resolved, and it will not be resolved by a press release.

Read next